Definition of “Scope”

For an effective GHG reduction management plan, setting operational goals for direct and indirect emissions will help organizations to achieve better GHG emission targets along its value chain*.

As defined by the GHG Protocol, to help define emission sources, improve transparency, and guide for different types of companies and different types of climate policies and business goals, four scopes (Scope 1, Scope 2, Scope 3, and Scope 4) are defined for GHG accounting and reporting purposes.

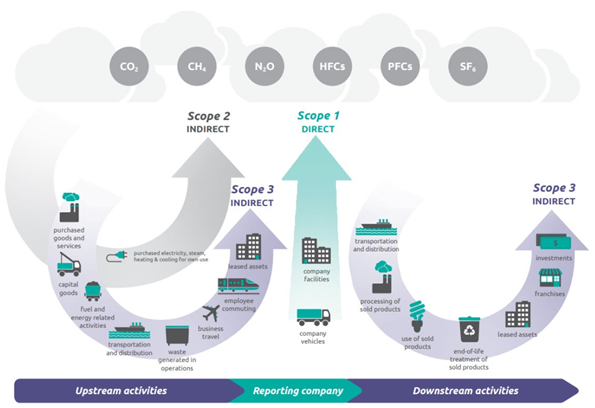

Figure 1 – Overview of GHG protocol scopes and emissions across the value chain

Source: WRI/WBCSD Corporate Value Chain (Scope 3) Accounting and Reporting Standard (PDF), page 5.

Scope 1 – Direct Emissions

Covers direct emissions from an owned or controlled source. Scope 1 emissions are divided into four categories:

- Stationary combustion (e.g. boilers, furnaces),

- Mobile combustion in company-owned vehicles burning fuel (e.g. cars, trucks, vans),

- Fugitive emissions (e.g. vent lines, leaks),

- Process emissions (e.g. production of CO2 during steel or other manufacturing).

Scope 2 – Indirect Emissions (Owned)

Covers indirect emissions from the generation of purchased electricity, steam, heating, and cooling consumed, including the emissions generated from the usage of electricity in the buildings of your organization. In other words, all GHG emissions released in the atmosphere from the consumption of purchased electricity, steam, heat, and cooling.

Scope 3 – Indirect Emissions (Not Owned)

Scope 3 emissions are referred as value chain emissions. This covers all other emissions that occur within the organization’s value chain, including the company’s suppliers and customers’ emissions. Scope 3 emissions include all sources not within an organization’s Scope 1 and 2, and include things like business travel, employee commuting, and emissions associated with the downstream use of a company’s product.

This is the biggest and the most difficult category for accurate data collection because the activities are typically farther along the supply chain, and accurate estimates often require data from trading partners like suppliers, vendors, distributors, and so on. Despite the difficulties associated with calculating these emissions totals,

IKEA, an international home furniture and furnishing retailer, has included Scope 3 emissions since 2016. The company’s Scope 3 emissions are almost fifty seven times higher than the sum of scope 1 and 2 emissions in the year 2021. While some companies like IKEA already do this reporting, a large majority other do not and/or do not have the systems in place to track these figures. Despite this, this reporting will only become more important for large corporations going forward, as a recent SEC proposal aims to require Scope 3 emissions reporting for large corporations in the U.S. by February 2025.

Scope 4 – Avoided Emissions

The most common use of the term Scope 4 emissions is to describe avoided emissions. According to the Greenhouse Gas Protocol, avoided emission reductions are those that occur outside of a product’s life cycle or value chain, but as a result of the use of that product.

Let’s use zoom meetings with clients for a software company as an example. These meetings are used to enable remote work for employees who would otherwise be commuting into an office to meet clients. The GHG emissions those employees AVOIDED by joining zoom meetings are Scope 4 emissions for this software company.

Some organizations are already setting goals around the climate change benefits of their products and services. Two-thirds of companies that report to the CDP (formerly known as the Carbon Disclosure Project) say the use of their products directly enable GHG emissions to be avoided by a third party.

The majority of reporting initiatives like the Science-based Targets Initiative and CDP don’t require organizations to report on avoided emissions. However, it will become an increasingly critical gap in disclosure, and reporting on it could potentially drive climate action among businesses.

Secondary Scope 4 – Emissions Associated With Working From Home

During the Covid-19 pandemic, there were discussions about the reduction of pollution and GHG emissions as a result of less travel and working from home.

Having a new lifestyle with the pandemic, there is an increasing rate of emissions associated with working from home. Although not as popular as using the term Scope 4, there are some articles using the Scope 4 term to also describe the emissions related with working from home. This new working style could lead to a small increase in emissions as a result of extra residential energy use, but when you take into account the number of employees working from home, this small increase can be turned into a large number.

Working from home will reduce energy demand for an employee that commutes by car. But for sure, commuters using public transport will increase energy demand. Taking this into account, findings show that the overall energy saved as a result of less commuting is still around four (4) times larger than the increase in residential energy consumption.

There are uncertainties about working from home for the long term. Over time, a shift to working from home could result a decrease of office spaces, consequently energy reduction for commercial buildings and GHG emissions.

To see how to calculate these emissions, you can refer to these resources for more information;

- EcoAct in partnership with Lloyds Banking Group and NatWest Group: Homeworking emissions Whitepaper

- International Energy Agency

*Value chain includes all activities that provide and receive value throughout the life cycle of a product or a service, from supply to disposal after use and includes aspects such as business models, investments, and stakeholders.